")

Long-term investors (shareholders) of MTN Ghana are expected to significantly benefit from the durable competitive advantage of the telecommunication company.

The company’s competitive advantage creates a monopoly-like environment that allows it to either sell more or charge more for its product/service.

The durability of the company’s competitive advantage has to do with the consistency in the company’s growing net earnings, assets value, return on equity etc over the past years – at least for the last 10 years.

MTN Ghana’s durable competitive advantage is driven by its dominant market share of the country’s telecommunication industry, unique product/service offering and large investments into innovation.

Driven by its competitive advantage, MTN Ghana has steadily grown its net earnings, market capitalization since listing on the Ghanaian bourse, return on equity, earnings per share and total assets value.

Net earnings of MTN Ghana over the last five years – from 2018 to 2022 – has grown from GHS 754.6m ($65.7m) to GHS 2.85bn ($248.2m) representing a 277.68% (+27,768bps) increase in net earnings.

Assets value over the same five year period has grown from GHS 4.21bn ($366.6m) to GHS 22.06bn ($1.92bn). In percentage terms, this marks an increase of 423.99% (+42,399bps). This compares favourably to the lower but increased liabilities of the company from GHS 1.80bn ($156.7m) in 2018 to GHS 16.35bn ($1.42bn) which indicates a 808.33% (+80,833bps) rise in liabilities.

Return on Equity (ROE) has also steadily risen from 39.31% to 53.54% over the five year period.

Shares of MTN Ghana listed on the Ghanaian bourse has witnessed a 100% (+10,000bps) increase in share price gain (capital appreciation) within the first five year of its IPO in September 2018 when a share cost GHS 0.75 ($0.065) to GHS 1.50 ($0.13) at end-August 2023.

Therefore driving the market capitalization of the equity from GHS 9.7bn ($844.7m) in 2018 to GHS 18.43bn ($1.60bn) at end-2022.

The GSE-MTN price chart showing the performance of MTN equity over the last five years

Dividend yield and price earning ratio (P/E ratio) which measures the company’s income paid to shareholders as dividends and how the shareholders value the company’s ability to grow its income stream respectively, have been a bit volatile over the five year period but have generally outperformed the industry’s average. Growth in earnings per share (EPS) has on the other hand, experienced a continuous rise over the five year period.

This chart shows the consistent growth in the earnings per share and earnings yield of MTN since 2019 and further into 2025.

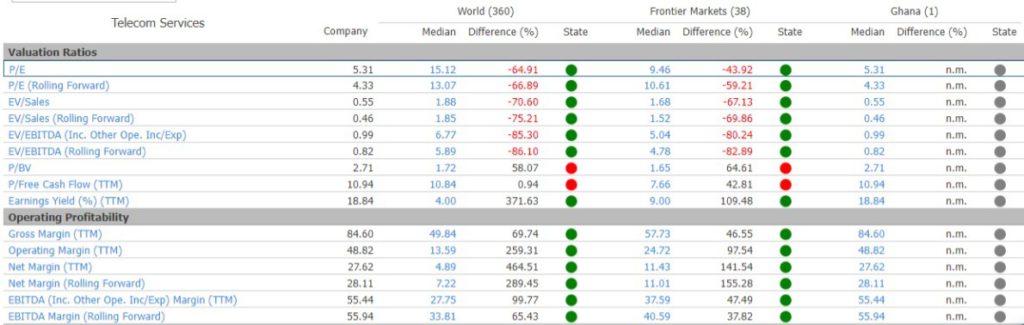

MTN Ghana given its long term competitive advantage outperforms peer telecommunication companies in frontier markets and around the world.

For instance, in dollar terms, Gross Profit Margin (TTM) for MTN Ghana is 84.6%, some 69.59% (+6,959bps) higher than the median Gross Profit Margin (TTM) of 49.89% for telecom companies around the world. It is also higher by 46.55% (+4,655bps) above the median 57.73% Gross Profit Margin of telecom companies operating in frontier markets.

This implies that, in terms of Gross Profit Margin, MTN Ghana has for the past twelve months performed better than almost half (49.89%) of telecom companies around the world and slightly more than half (57.73%) of telecom companies in frontier markets. Gross Profit Margin indicates how efficiently a company manages its costs and generates profit from its revenue. With a Gross

Profit Margin of 84.6%, MTN earns as gross profit 84.6 cents from every $1 revenue it makes.

Also in dollar terms, Net Profit Margin (TTM) for MTN Ghana is 27.62%, some 480.88% (+48,088bps) higher than the median 4.75% Net Profit Margin (TTM) for telecom companies around the world and 141.54% (+14,154bps) above the median 11.3% Net Profit Margin (TTM) for telecom companies in frontier markets.

This also implies that MTN Ghana for the past twelve months in terms of Net Profit Margin performs better than most telecom companies in frontier markets and around the world. MTN Ghana’s Net Profit Margin of 27.62% indicates that after accounting for its expenses including taxes, it earns as net profit 27.62 cents from every $1 revenue made.

Market Share and Shareholders

The company’s market share of the industry has steadily increased from around 46% in Q4 2015 to 66.6% at end-2022 with total subscriptions of 26.61 million out of the 40.04 million industry-wide subscriptions.

Vodafone, AirtelTigo and Glo follow with market shares of 18.82% (7.54m subscriptions), 13.95% (5.59m subscriptions) and 0.77% (0.31m subscriptions) respectively.

MTN also dominates the mobile data sector with 16.74m subscriptions representing 73.29% market share at end-2022 with Vodafone, AirtelTigo and Glo having 14.05% (3.21m subscriptions), 11.95% (2.73m subscriptions) and 0.70% (0.16m subscriptions) market shares respectively.

Risk to Competitive Advantage

The designation of MTN as a Significant Market Player (SMP) by the country’s telecom regulator, the National Communications Authority (NCA) poses a risk to the telecom giant’s competitive advantage.

A breakup of MTN’s industry dominance by the NCA through the implementation of its SMP measures will negatively affect the company’s competitive advantage impacting its operations and hence profitability.

The impact of the SMP directive by the NCA is, however, expected to last in the short to medium term. In the long term, MTN Ghana is expected to regain industry dominance given the seemingly general preference for the yellow brand by subscribers underpinned by the company’s ability to introduce innovative products/services that attract subscribers.

The regulator has defended its decision to designate MTN Ghana as a SMP asserting it allows the NCA to impose certain regulations and measures on MTN to prevent abuse of its market power and ensure fair competition.

By implementing measures such as asymmetric interconnection rates, tariff parity, and technology neutrality, the NCA aims to promote competition among the telecoms in the country, encourage innovation, and protect consumers’ interests. These measures, the NCA argues, will enable the other telecom companies to compete effectively, offer sustainable pricing, and invest in improving service quality.

Recommendation: Given its market dominance, increasing year-on-year profitability and long term competitive advantage, Ghanaian retail investors, institutional investors as well as Asset Management Firms are encouraged to include equities/shares of MTN Ghana in their investment portfolio.

To enjoy significant returns in the form of capital appreciation/gains (by several hundred percentage points) and higher dividends, investors are encouraged to adopt a long term horizon investment approach and hold MTN equities for the next 10, 15 and even 20 years.

Data used in the write-up are sourced from EquityRT, a research-focused platform with global coverage on equities.

The writer is certified by the Chartered Institute for Securities & Investment (CISI), UK, and the Ghana Investment and Securities Institute (GISI).

ALSO READ:

{kind=link}